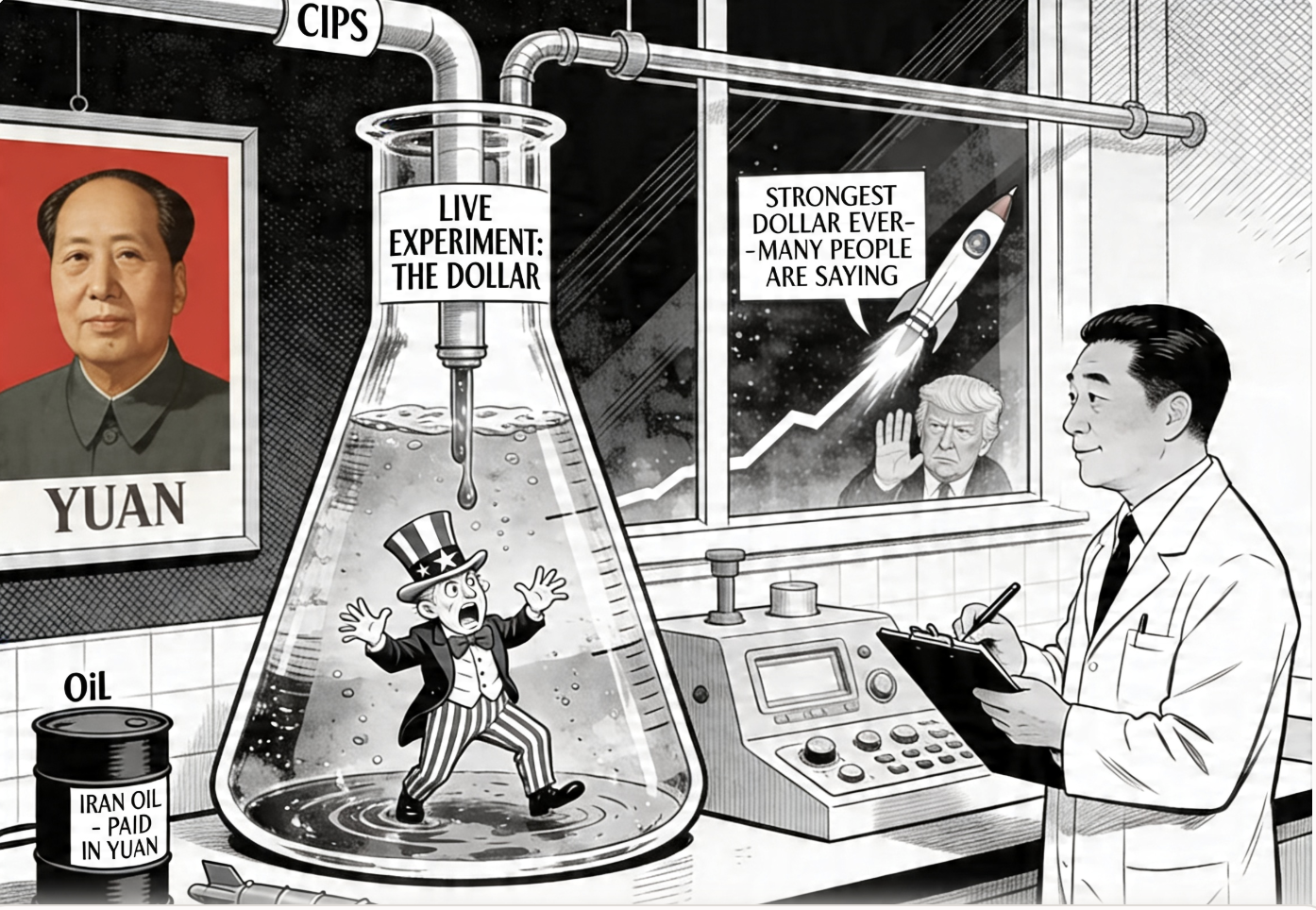

China has for years been telling the rest of the world it was building an alternative global financial system. Financial journalists used to scoff, but not any more.

Every barrel of Iranian oil that flows to a Chinese refinery, paid for in yuan and beyond the reach of the US Treasury, is a live demonstration that Beijing’s parallel monetary system does exactly what it was designed to do — function under maximum geopolitical pressure. Washington has sanctions. China has plumbing. The plumbing is winning.

The Test That Beijing Needed

China has been the largest buyer of Iran’s seaborne oil for decades, taking more than 80% of Iranian crude exports — roughly 1.4 million barrels per day — all settled outside the dollar system. When US strikes escalated the conflict in early 2026, the system did not crack. Iran pushed at least 11.7 million barrels through the Strait of Hormuz bound for Chinese ports, with payments flowing in yuan without a single dollar changing hands. In March 2026, China’s cross-border payment network recorded a single-day settlement of $178.5 billion — a direct consequence of the Iran war oil surge.

A live system, stress-tested by war, functioning at scale.

Meanwhile, Iran has quietly let it be known that it could accept toll payments from ships crossing the Strait of Hormuz in either cryptocurrencies or yuan. The country that sits astride the world’s most critical oil chokepoint is no longer asking to be paid in dollars. That is not a footnote. That is a headline.

The Weapons Loop

The financial relationship has a military dimension that makes it structurally self-reinforcing. Before the war started, Iran was near completion of a deal to purchase Chinese CM-302 supersonic anti-ship missiles — weapons capable of threatening US Navy aircraft carriers and destroyers at 290 kilometres range — along with surface-to-air and anti-ballistic systems. Six Iranian government and security officials confirmed the negotiations to Reuters; China officially denies knowledge. The deal would breach a UN arms embargo reinstated in 2025.

The logic of this arrangement is elegant and dangerous. Iran sells oil to China in yuan. Those yuan fund arms purchases from China. China arms the nation that controls the Strait of Hormuz. Every transaction deepens the loop, and bypasses the dollar entirely. Washington’s ability to sanction its way to compliance is being engineered out of the system.

Into this geopolitical chess match steps Donald Trump, who marked the early weeks of the Iran conflict by posting on Truth Social that the US had “the strongest dollar in history, maybe ever, possibly the greatest ever, lots of people are saying it.” The yuan’s share of Iran’s oil settlement that week: 100 percent.

The Infrastructure Is Already There

The Iran crisis did not create this system. It merely stress-tested infrastructure that has been quietly assembled over a decade. At the heart of it is CIPS — the Cross-Border Interbank Payment System — China’s direct answer to SWIFT, the Brussels-based messaging network through which virtually all international dollar transactions flow and which the US has repeatedly weaponised as a sanctions tool. Where SWIFT reports transaction data to its board of Western central banks and is subject to US legal reach, CIPS operates entirely under Chinese jurisdiction, uses its own internal messaging protocol, and makes transactions invisible to Western monitoring. It is not a workaround. It is a replacement.

China began construction of CIPS in 2012 under the direct supervision of the People’s Bank of China, launching Phase 1 on 8 October 2015 with 19 direct participants and 176 indirect participants across 50 countries. Beijing understood from the start that the system would only gain legitimacy if it recruited Western names. The first wave of direct participants included Citibank, BNP Paribas, and Deutsche Bank — household names of the same financial order China was building to overthrow. HSBC, Standard Chartered, DBS, and ANZ followed, becoming shareholders in CIPS Co. Ltd itself. These were not reluctant recruits; they were chasing yuan-denominated business and saw CIPS as commercially essential.

The first true “whale” — a non-Western institution of systemic global significance — came as the Gulf states began hedging against dollar dependency. The most recent, in June 2025, was First Abu Dhabi Bank, the UAE’s largest lender, which became the first MENA bank to join CIPS as a direct participant. That a bank at the heart of the petrodollar system — in the nation that anchors Gulf oil dollar recycling — has now plugged directly into China’s yuan settlement network is perhaps the single most telling data point in the entire de-dollarisation story.

The broader architecture built around CIPS is equally formidable:

-

CIPS now connects 193 direct participants — up 40% since 2024 — with banks bypassing SWIFT entirely using its own internal messaging protocol

-

Project mBridge, the multi-central-bank digital settlement platform linking China, Saudi Arabia, UAE, Thailand, and Hong Kong, has processed more than $55.5 billion in trade, a near-exponential rise since 2022

-

The digital yuan (e-CNY) hit $2.3 trillion in cumulative transactions in 2025 and became interest-bearing in January 2026 — making it a genuine store of value, not merely a payment token

-

Yuan’s share of China’s own trade settlement has risen from 28% in 2020 to 64% in 2024

-

Hong Kong banks have doubled permissioned access to onshore Chinese liquidity as demand for yuan-denominated loans surges from Gulf and Central Asian clients

As analysts at the Council on Foreign Relations have noted, the apparent decline in the yuan’s share of SWIFT data is misleading — it does not mean less usage, it means trade messages have gone private and become invisible. The system has not shrunk. It has gone dark.

What This Means for Western Economies Drowning In Debt

Here is the consequence that almost no Western politician is willing to articulate publicly. The dollar’s reserve status has functioned for decades as a hidden subsidy to Western governments — allowing the US, UK, and eurozone nations to borrow at artificially suppressed interest rates and run structural deficits that would otherwise be unsustainable. That subsidy is now being withdrawn, systematically and deliberately, one yuan-settled transaction at a time.

If China succeeds in anchoring global oil, arms, and trade settlement in yuan — a threshold Iran may have already pushed it past — the cost of borrowing for Western governments rises. Debt servicing crowds out public spending. To maintain welfare commitments, taxes must increase. To keep taxes politically bearable, spending must be cut. The mathematics of de-dollarisation does not lead to a polite currency realignment. It leads to the fiscal dismantling of the postwar welfare state.

The Institute for Fiscal Studies already warned of structural UK spending gaps running to tens of billions annually before any dollar credibility shock. A genuine reserve currency transition would not add pressure at the margins. It would collapse the fiscal assumptions on which the NHS, state pensions, and social security are all built.

China Keeps Its Promises

There is one further lesson that Western governments and media have consistently failed to absorb: China does what it says it will do.

While Washington reversed course on trade deals, multilateral commitments, and security guarantees with bewildering frequency — most recently abandoning its own stated red lines on Iranian facilities — Beijing has executed its financial architecture project with patience, consistency, and precision over more than a decade. The alternative payment system it promised is built. The oil settlement mechanism it promised works. The weapons it promised Iran are nearly delivered.

Which brings us to Taiwan. In 2024, Chinese officials made clear, in terms more explicit than at any previous point, that reunification with Taiwan would be completed by 2027. The Western foreign policy establishment responded much as financial journalists once responded to China’s monetary ambitions — with a mixture of dismissal and performative concern. That was a mistake then. It would be a graver mistake now.

A look at the “dollar vote” provides perhaps the most compelling evidence of all: Taiwanese stock TSMC now constitutes a larger share of the MSCI EM index than all the stocks in India put together. Please use the sharing tools found via the share button at the top or side of articles. TSMC is the most widely held stock, owned by 92 per cent of global equity funds. In comparison, Microsoft, the most widely owned US stock, is held by 84 per cent of those funds.

If the Iran experiment has demonstrated anything, it is that China’s strategic announcements are not bluster. They are timetables. The world has just watched Beijing prove its financial system works. It would be wise to take equally seriously what it says it intends to do next.

Fact-check note: Iran-China CM-302 supersonic missile deal confirmed near-completion by Reuters citing six Iranian officials, February 2026. No delivery confirmed. China denies official knowledge. Deal would breach reinstated UN arms embargo. First Abu Dhabi Bank CIPS direct participation confirmed June 2025.